A survey by the business information service Lexis Nexis finds that consumers have grown more wary of programs that ask them to share data in exchange for improved services or other offerings.

Editor’s note: LexisNexis has clarified that its survey was released in August, 2013, not October, 2013. The story has been corrected to reflect that information. – Paul 6/4/2014

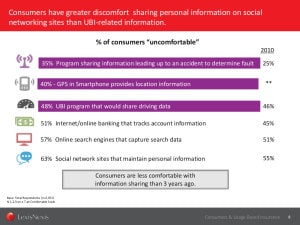

The survey of 2,072 consumers, aged 21 to 74, was conducted in October 2013 by LexisNexis Risk Solutions. It found consumers were more wary of sharing information online, including at social networking and online banking sites than they were three years earlier. “Consumers are less comfortable with information sharing than three years ago,” the survey concluded.

The survey was released in concert with Telematics Detroit 2014, a conference focused on information systems used in vehicles. It was designed to measure consumers’ awareness of- and interest in so-called “use based insurance” (or UBI) – sometimes referred to as a ‘pay as you drive’ insurance programs. Among its other conclusions, it revealed growing awareness of such programs, which use data on driving behavior for individual drivers to tailor insurance rates.

[Read more Security Ledger coverage of security and privacy issues in the insurance industry.]

One in every three consumers surveyed in 2013 was aware of usage-based insurance (UBI), or telematics, LexisNexis reported. That’s triple the percentage of surveyed consumers who were aware of such programs in 2010.

“While still a novel concept for many consumers, usage-based insurance programs offered by car insurers to track driving habits are becoming more mainstream, less unique than they were three years ago,” LexisNexis said in a published statement.

But questions that asked about consumers’ comfort with information sharing programs sound a cautionary note about the future of services like use-based insurance. Thirty-five percent of those surveyed reported being “uncomfortable” sharing information leading up to an accident with insurers in order to determine fault. Three years ago, just 25% said they were uncomfortable with that notion. 48% said they were “uncomfortable” with UBI programs that share driving data, an increase of 2% since 2010. And 40% of those surveyed said they were uncomfortable with GPS data from a mobile device being used to provide location information to their insurer.

The feedback on user-based insurance was consistent with respondents’ feelings about other, more common types of data sharing. Fifty-one percent of those surveyed were uncomfortable sharing Internet or online banking services that track account information, up from 45% in 2010. And 57% of those surveyed said they were uncomfortable with “online search engines that capture search data” – up from 51% three years ago. Fully 63% surveyed reported being uncomfortable with social network sites that collect personal data, up 8 percentage points from 2010.

The insurance industry is poised for technology fueled disruption as homes and automobiles become connected to the Internet of Things. In the case of automobile insurance, insurers will ultimately have to wrestle with questions of liability with autonomous vehicles. In the near term, realtime or near-realtime data on driving behaviors and the operating condition of vehicles will provide a wealth of previously unavailable data to insurers that will allow them to fine-tune their actuarial calculations about the risk of an accident. However, such data also poses a major challenge to insurers to protect the privacy of their customers. In just one recent example, researchers were able to show that UBI technology that tracks driving behaviors can also be used to determine where a particular vehicle has been driven – without the use of GPS data.

The study found consumers willing to try UBI programs, especially where discounts are offered in exchange for participation. 50 percent of consumers said they would be “likely to sign up” for a use based insurance program in exchange for a 10 percent discount on rates.

But even those figures reveal a wariness on the part of the driving public. Among the factors most likely to increase their interest in trying out a use-based insurance program, the most oft-cited was the ability to “opt out without a penalty” (80%). The ability to choose what information to share (cited by 77%) and guarantees that the collected data would only be stored for a short time (69%) rounded out the top five factors for those responding to the survey.